TL;DR - Directionally correct move that we support in the immediate term, but we believe PoG remains the clearest path to durable, value-accretive token economics.

These are our high-level takeaways:

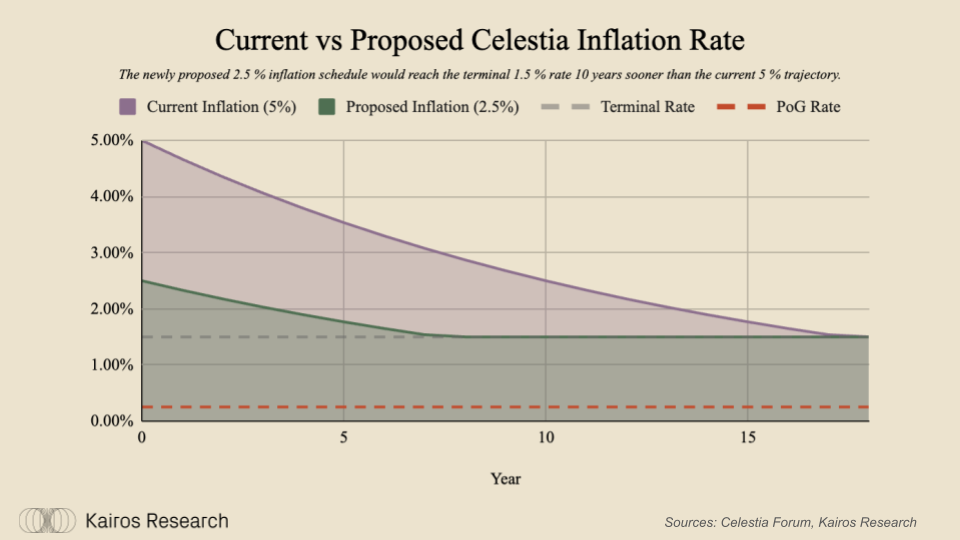

• Issuance Implications: Halving base inflation from 5% to 2.5% removes ~29m of new TIA tokens each year and trims eight-year issuance by ~220m TIA, bringing the 1.5% terminal inflation rate forward by a full decade.

• Validator economics: Raising the commission floor to 10% lifts the stake-weighted fee from 14.2% to 16.5%

54 validators (~55% of stake) must adjust, shifting about 0.7m TIA per year from delegators to operators, small on a network-wide basis, but meaningful as rewards shrink.

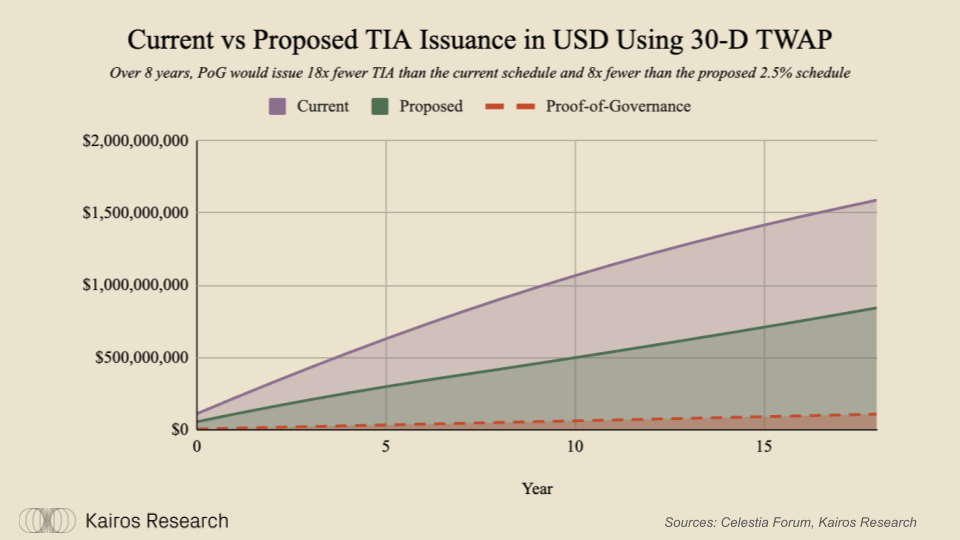

• PoG Remains the Optimal Economic Path: In our opinion while this is a directionally correct move for issuance policy, PoG’s 0.25% inflation track still dominates on long-term scarcity.

Over eight years it mints about eight-times fewer TIA than the newly proposed schedule, pushing the network close to neutral issuance while leaving headroom for DA-fee growth and other potential avenues to do the heavy lifting.

We believe PoG remains the clearest path to durable, value-accretive token economics.